Applying for a loan is a major step and one where small mistakes can derail approval. Avoid these common loan application mistakes to secure the financing your business needs.

Review your credit profile and debt-to-income ratio, avoid new credit applications (which may affect your score) and prepare all requested documentation in advance. Working with a financial professional can also strengthen your loan application and help you navigate the process smoothly.

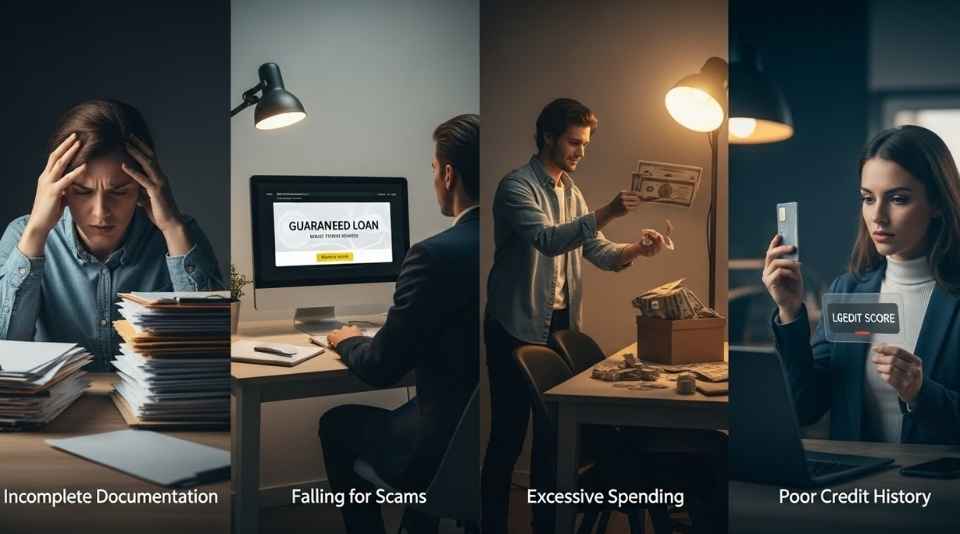

1. Not Reviewing Your Credit

A person’s credit history is a key factor in getting approved for a loan, whether it’s for a home, a car, or money for college. It’s important for potential borrowers to understand how the loan application process works so they can avoid common mistakes that could derail approval.

A borrower’s financial track record is captured in their credit reports from the three major credit review companies (Equifax, Experian, and TransUnion), which contain information about lenders that extended them credit in the past. This data includes payment history, the balances on their loans, and other details. The credit reviews are combined to create a score, which is used to determine the creditworthiness of a borrower.

Having an outstanding debt, bad credit, or a low credit score can lead to denial of a loan, or at least higher interest rates and terms. To ensure that you have the best chance of loan approval, it’s wise to take steps to improve your credit before applying. This can include paying down existing debt, using a debt snowball or debt avalanche strategy to make payments on time, and not opening too many new forms of credit.

In addition to a borrower’s credit, lenders also look at their income and employment status to ensure that they can afford the repayment of their loans. This is done by calculating their debt-to-income ratio, which is the amount of debt they have compared to their monthly income. To help a potential borrower demonstrate that they are responsible, having consistent income and no significant employment changes are key factors in winning loan approval.

If a borrower receives a denial of loan application, it’s important to find out what was the main reason so they can correct the issues and try again. If the lender cites an error on their credit report, it’s up to the borrower to dispute this with the credit reporting company and the source of the erroneous information.

Applying for a loan can feel stressful, especially if you’ve been turned down in the past. However, understanding the top loan application mistakes to avoid can help you secure a personal loan with confidence.

2. Not Comparing Lenders

Whether you’re launching a startup, expanding with commercial real estate, or needing working capital to manage growth, the right loan can make all the difference. But securing financing isn’t always simple, and first-time borrowers often make avoidable mistakes that slow down or derail their application. Understanding these common missteps can help you proactively improve your approval odds and secure more favorable loan terms.

A key mistake is applying to multiple lenders without a clear strategy or well-documented business plan. Submitting multiple applications triggers multiple hard credit inquiries, lowering your business’s credit score and raising red flags for underwriters. Instead, carefully research the lenders that match your business needs and qualify you based on the information provided in the prequalification process.

It’s also a mistake to focus only on the interest rate when reviewing different loan offers. In addition to the interest rate, be sure you understand how fees impact your total borrowing costs. Lenders are required by law to present these costs using annual percentage rates (APRs), which include both interest and any fees that must be paid. Compare these APRs between different lenders to determine which one best meets your borrowing needs.

Another mistake is applying for a loan amount that’s too large for your budget. This raises the risk of repayment default and reduces your lender’s confidence in your ability to handle a debt payment. Use loan calculators to estimate the cost of each option and choose an amount that aligns with your budget and long-term financial goals.

Finally, a big mistake is failing to provide thorough, accurate, and consistent loan documents. Lenders look for clarity around ownership details, business plans, revenue projections, and the loan purpose. These documents are reviewed closely during the underwriting process, and even small inconsistencies can raise red flags for underwriters and slow your approval.

Ultimately, successful borrowers are those who take the time to review their personal and business credit, clarify their loan purposes, apply for a loan with one or two lenders, and thoroughly review and negotiate their final terms. By avoiding these common pitfalls, you can speed up your business loan approval and feel confident that the financing you receive is the most competitive available.

3. Not Reviewing the Loan Documents

A loan can be the lifeline needed to reach a business’s growth potential. However, mistakes can derail the process. This can include anything from clerical errors to serious financial discrepancies that signal risk.

It is important to carefully review the loan documentation and all associated materials before applying for a business loan. It is also important to understand all fees, repayment terms, and penalties for default. Many borrowers overlook these details when making the application, and can end up paying more in interest costs than they need to.

A lender’s underwriter rely on their experience and knowledge of credit to evaluate each loan request. Even a minor error can impact the underwriter’s comfort level and negatively affect approval chances, terms, or interest rates. This is why it is important to have your documentation in order long before you start the application and to make sure all documentation, projections, and narratives are up to date.

If there are any blemishes on your credit, be prepared to explain them and be ready to provide additional documentation or to sign a letter of explanation (LOE). This is a common practice and usually not a big deal. However, if you are hiding information or trying to hide a bad debt history, it can be very difficult to get the loan you need.

Lenders are looking at the complete picture and evaluating your ability to repay the loan. If there is any doubt, it could result in the loan being denied or the terms being severely negotiated. This can be costly for a business that is counting on the loan to grow.

Whether you are launching a startup, expanding with commercial real estate or buying equipment, a business loan can be an important investment in your company. Avoid the top mistakes when borrowing money and you can have confidence that your loan will be a success. For more information on how to successfully secure a loan, contact Redbridge today and set up time with a funding expert!

4. Not Communicating With Your Lender

The accuracy and completeness of your loan application directly impacts the quality of funding offers you receive. Whether it’s bank lending, equipment financing or alternative business loans, errors, omissions and inconsistencies are among the most common reasons entrepreneurs face delays, denials and unfavorable terms on their applications. Mistakes can range from simple clerical issues to financial discrepancies that signal risk.

Inflated financial claims, a lack of cash reserves and inaccurate revenue and expense projections all reduce lender confidence in the business’ ability to repay debt. This can lead to rejection or strict loan conditions that make it difficult for the business to thrive and meet repayment obligations.

Lenders are more comfortable working with borrowers they’ve built relationships with. Personal connections can also help borrowers craft a narrative that generates support in loan committee meetings. Taking the time to build banking relationships early and telling a clear, consistent story can save valuable time in the loan process and increase the likelihood of a successful outcome.

Lastly, it’s critical to clearly communicate your funding needs and funding goals with the lender. This prevents confusion about the purpose of your loan and ensures the loan is structured to match your specific business needs. Inaccurate information can lead to unnecessary delays and can even result in rejection if the lender reports discrepancies to credit bureaus, which can damage your business’s creditworthiness and affect your ability to obtain future loans or credit.

Avoiding these top loan application mistakes is the best way to set your business up for success when applying for funding. To streamline the process, review your credit and choose a lender that is the right fit for your unique business needs. It’s also important to only submit loan applications that are required by the lender and to do so in a timely manner. This helps you avoid multiple hard credit inquiries that can damage your credit score and trigger unwanted marketing from lenders (also known as trigger leads). To avoid these common mistakes, take the time to review your credit and understand the business lending process to avoid costly delays and rejections.